If you read our last blog you are somewhat familiar with the different ways financial advisors make money ie-collect fees. We will go into a bit more detail on each way an advisor can make money.

Transparency is very important. You should know what you are paying your financial advisor and how you’re doing so.

When you start to look at the ways advisors get paid you’ll notice there are commissions, fee-based, and fee-only. Before we jump into the nitty gritty around compensation, let’s get a few common terms defined for you-assets under management, conflicts of interest, and fiduciary.

Let’s start with assets under management (AUM). This means the fee that is being charged, is for the assets (accounts) that the financial advisor is managing the investments on. An example of this would be if you set up an IRA with this financial advisor and they are deciding on the investments inside this IRA, then most likely this account would be included in the fee for assets under management. Now, let’s say you have a 401(k) and the financial advisor is NOT managing those assets, then this account would most likely not be included in the fee for assets under management (always confirm this is the case).

Conflicts of interest are well, pretty straightforward, or are they? A conflict of interest is a situation where the advisor’s personal interest could compromise their judgment, decision, or opinions on a client’s situation. You get it? We agree this one definitely needs a few examples. Let’s say a financial advisor gets paid $5 for using XYZ companies’ annuities and gets paid $10 for using ABC companies’ annuities. Well this creates a conflict of interest as it could create a situation where the advisor doesn’t share XYZ annuity with the client because they will get paid more for the ABC annuity. This does not mean that the higher commissioned product is bad,, it just means that the advisor should disclose this conflict of interest and share information on both annuities and let you, the client, decide.

Let’s go through one more example to really make this clear as mud! Investment advice could be a conflict of interest. Let’s say a financial advisor is managing your investments and uses all RST funds because they pay a commission to the advisor. Again, does not mean that RST funds are bad, it just means that the advisor should be disclosing this conflict of interest with an explanation on why they use these funds.

Fiduciary-you hear it often; however, do you really know what it means? A financial advisor who is a fiduciary is legally obligated to act in the best interest of their client at all times. Another way to put this is that your interests (the client) are ahead of the financial advisors interest. Fiduciary Financial Advisors have a duty of care and duty of loyalty to you, the client. Duty of care means the advisor takes in consideration all aspects of your (the client) situation before making recommendations. Duty of loyalty means the advisor acts as a fiduciary at all times of engagement with the client and to disclose any conflicts of interest that may arise.

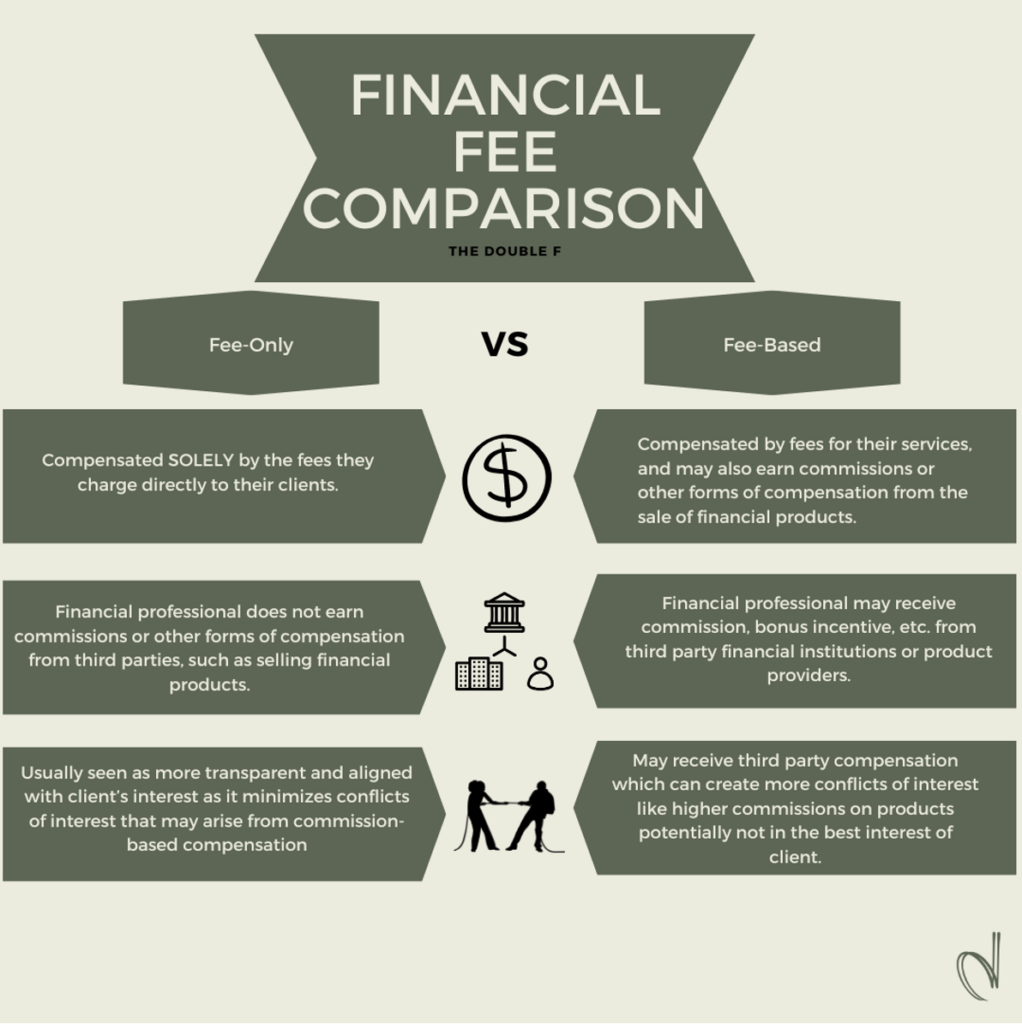

Ok, now that you are a guru with understanding AUM, conflicts of interest and fiduciary, let’s move on to the Double F in fees. Fee-Based and Fee-Only.

What are the differences?

Fee-Based are typically financial advisors who charge fees for their services, and who may also earn commissions or other forms of compensation from the sale of products to clients. Commissions can be on investment products (ie. mutual funds), or financial products such as annuity or life insurance contracts. These commissions are paid by third parties, such as institutions or product providers.

This is not necessarily wrong or bad; however, it is something you as the client should be aware of. Why? Because it can cause some conflicts of interest between you, the client, and the advisor. It’s best to ask the advisor to disclose all conflicts of interest so you can understand what conflicts arise by being their client. An example is if you are working with an advisor who recommends an annuity product and only presents an annuity product from one company. This could be a case where they are beholden to the product company and therefore cannot recommend outside product providers which may have better products to suit your needs.

Fee-Only are typically financial advisors who are compensated only by the fees they charge their clients for their service. These fees can be charged in different ways. For example you could be charged hourly, a flat rate, or a percentage of the assets the advisor manages (AUM). Essentially any of these fees are paid directly by you, the client, to the advisor. The advisor does not earn any commission or any other form of compensation from any financial institutions or product providers.

This tends to reduce the amount of potential conflicts of interest because the advisor has no incentive to recommend certain products over others based on the commission they would earn from that product. It also creates transparency as you, the client, knows exactly how much you are paying for the service you are receiving. Typically, you will find this type of arrangement aligns well with the client’s best interests as their compensation structure is not tied to specific financial products.

The other compensation model to understand is commission based.

Commission based compensation means that the advisor is going to be compensated with a commission on the product or investment they sell. An example would be an insurance policy. Let’s say you purchase a life insurance policy from a financial advisor who is not fee-only. The financial advisor is most likely earning a percentage for the sale of this product. You, the client, do not pay this out of pocket, the insurance company pays the financial advisor. Another example could be investment related. The advisor sells you a certain mutual fund and earns a percentage of that sale.

To be completely honest no fee structure is perfect in our opinion. What matters the most is that your financial advisor is a fiduciary at all times, that you understand how you are paying them for their advice, and any conflicts of interest are disclosed. Once you have all of this information you can make an informed decision on if that aligns with your needs.

Check out the diagram below for an easy to digest breakdown of Fee-Only & Fee-Based. As always, reach out with any questions and don’t let the world of fees overwhelm you.